BofA Just Threw Up All Over The Fed''s "Transitory" Argument: Here''s Why

BofA Just Threw Up All Over The Fed's "Transitory" Argument: Here's Why a day ago

![]()

4 images

One look at the recent collapse in 10Y breakeven rates, which have tumbled 24 bps to 2.37% since their May 12 peak despite today's red hot CPI print...

... could convince even the most hard-core bond bears that investors have likely committed to the Fed’s "transitory" inflation narrative, and now subscribe to Powell’s labor market maxim, that a recovery in American jobs is more important than inflation concerns right now (even if other labor market indicators such as job openings hints at much tighter conditions) and that no hikes are coming for a long, long time.

And yet, the evidence of shortages and inflation continues to grow with every passing day, as does the list of reasons to dismiss the problem as purely temporary, although as even BofA economists note in their daily note, "judging from the non-reaction of markets— with 10-year yields dipping back below 1.5% and the stock market near record highs— those arguments are winning the day."

BofA's response was simple: as the bank's chief economist Michelle Meyer said "we don’t buy it", noting that as signs of shortages and inflation continue to arrive, including several warnings this week, "individually the arguments for complacency make sense; collectively they are becoming increasingly unconvincing"; it's also why Meyer continues to believe that "the groundwork for more sustained inflation down the road is building."

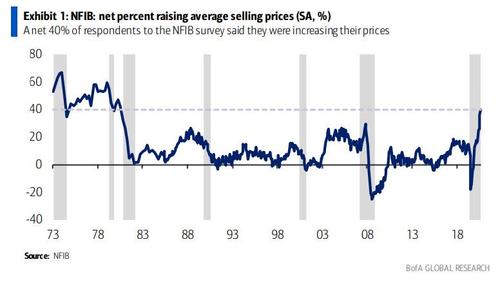

She does have a point - after all, just this week, we found that both the small business survey and the “JOLTS” data showed a significant escalation of the shortage problem in May. All of the small business questions around prices, wages and shortages worsened on the month. For example, a net 40% of respondents said they were increasing their prices, marking the highest reading since 1981

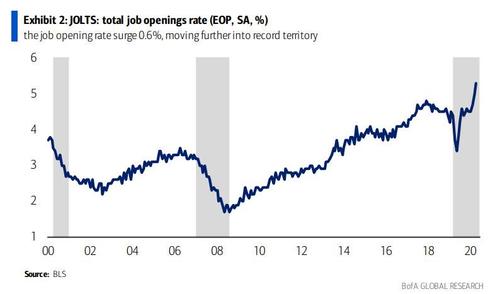

Similarly, the JOLTS data lived up to its name, as the job opening rate surged 0.6%, moving further into record territory while a record number of Americans quit their jobs.

But instead of highlighting the inflationary dangers signaled by these indicators, when digging around in the business press, we instead find a growing list of excuses for the shortages and signs of inflation. As you skim through the list below, keep in mind not only the evidence of shortages, but also the fact that average hourly earnings have risen at 7.4% annualized rate in April and May and core CPI inflation is likely even higher. Here, courtesy of Meyer, is the laundry list:

Labor shortages will vanish in the fall when unemployment benefits drop, childcare becomes more available and fear of getting COVID on the job fades.

Bottlenecks in goods production are due to idiosyncratic shocks. They will fade as production picks up and as demand shifts from goods to services.

Bottlenecks in trade will also ease as the impact of past disruptions fades, labor shortages ease and demand for goods stops growing so fast.

The rise in prices is purely temporary and sector specific. It will go away as supply picks up.

Any pick-up in price inflation is by definition temporary because there is still an output gap and sustained price pressure requires closing the gap.

The rise in wages is mainly in low-wage jobs. That is a good thing because it helps close some of the income gap.

The link between wage and price inflation has weakened in recent years. Again, we should celebrate not bemoan the rise in wages.

Any increase in wage growth is by definition temporary because the unemployment rate is still too high to generate sustained wage pressure.

The Michigan measure of inflation expectations has surged, but that is an overreaction to highly visible food and energy price increases and will fade when they fade.

Historically, inflation expectations only rise after there is a sustained period of high actual inflation. The recent rise must be a fluke.

Inflation breakevens have only risen modestly and if there was a real inflation problem the bond market would tell us.

Ignore these rough survey measures of inflation expectations. Surveys of professional economists still see inflation meeting the Fed’s target in the long run.

And then, Meyer points out the coup de grace: "don’t worry about inflation getting too high, the Fed can raise interest rates as much as needed to cool inflation." Sure it can... It can also crash the precious stock market in 15 minutes.

So why is Bank of America worried?

Because, as Meyer correctly notes, there is some truth to all of these arguments, but it is implausible to argue that all of the recent inflation problems are temporary, and most important these “temporary” pressures will probably persist for many months and could become embedded in inflation psychology. This is particularly likely given that monetary and fiscal authorities have demonstrated in word and action that they want a red hot economy and rising inflation in the next few years.

Meyer also disagrees that the Fed can easily put the inflation genie back in the bottle: "we haven’t had sustained high inflation in recent decades, but older history shows that once it gets going it is hard to contain without triggering a recession."

Moreover, the Fed’s current policy strategy makes it even harder, as they are promising to tighten later than normal and only when they are convinced that higher inflation is embedded in the economy.

Meyer's conclusion: while investors fear the day that the Fed signals rate hikes ahead, ironically it would be better for the sustainability of the expansion - not to mention risk assets - if that signal comes a lot earlier than the Fed is currently suggesting, at which point it will be too late...

Tyler Durden Thu, 06/10/2021 - 17:30