RioCan REIT: A Compelling Profile Despite The Pand...

Introductory Investment Thesis

RioCan (OTCPK:RIOCF) is one of Canada's largest real estate investment trusts (REITs). The latter owns and operates mixed-used properties located in different key cities that involve offices and shops. Toronto remains the main driver at 51% of rental revenue as of Q3-2020 followed by Ottawa (12%), Calgary (11%), Edmonton (7%), Vancouver (5%) and Montreal (4%).

As evidenced with the COVID-19 wave, many investors are wondering if the REIT is still a good investment especially considering the population density in Toronto. While EBITDA is clearly under pressure from the pandemic crisis, the REIT looks well positioned to recover post COVID-19. That's considering the favorable dividend payout and discount valuation multiple that the REIT is displaying. We'll be looking in this article at some of the attractive characteristics of this REIT, including the resilience of its Q3 results, balance sheet strength and discounted unit price. Against these strengths, risks of a dividend cut shouldn't be excluded and I believe the stock won't outperform in the near term.

Decent 3rd quarter considering the pandemic environment

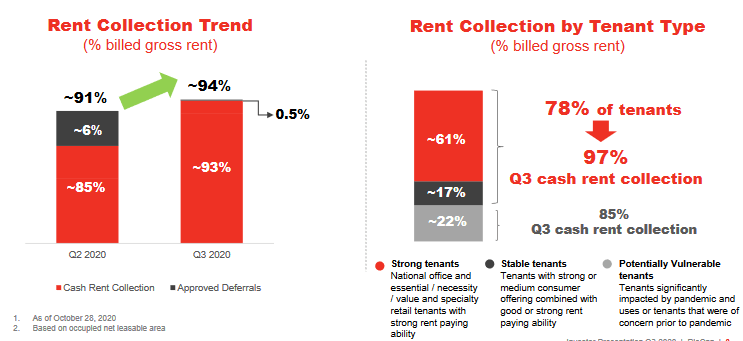

Most key financial measures for RioCan improved at Q3 compared to Q2 which entails some resilience given the extent of the pandemic crisis. In fact, the FFO per unit growth of $0.06 represents a 17.2% increase quarter on quarter and RioCan has been able to collect 93% of its rent while maintaining around 96% in occupancy rate (Source: Financial Post release). This translates into an 8% collection increase vs. Q2 - a mark of income sustainability we should acknowledge. Considering that several tenants resumed activities during Q3, that is not surprising. In Canada, the recent closures including gyms and restaurants lead me to think that collections might revert towards Q2 levels.

Reflective of the better Q3 standards, the provisions for rent abatements and bad debts declined from 6.8% to 5.3% of total billed rents quarter-on-quarter. Of note, the collections included the government funding received under the assistance program (CECRA) which - in essence - represented only 2.5% of total rents in Q3-2020.

Looking at RioCan's supplementary information, management segregated rent collections by tenant category. 78% are deemed strong or stable tenants while 22% are considered potentially vulnerable. Bearing in mind collection rents, the 22% portion must not be confused with defaulting companies as only a low portion of tenants are filing for bankruptcy. More so, closure represented a marginal portion of the REIT's annualized rental revenues (<1%). In other words, RioCan is still expecting to collect the majority of its revenues under that vulnerable category.

In addition, I'd like to point out that the residential operations performed well as RioCan collected strong revenue from its rental operations (i.e., eCentral, Frontier & Brio). In Toronto, eCentral's lease rate stood at 92.1% while the project 'Brio' in Calgary - launched in the middle of the pandemic - averaged 52.5%. While this rate requires caution, it still shows management had a strong leasing ability despite the impact of the crisis - keep in mind Calgary has also been impacted by oil prices.

On a final note, RioCan predicts an FFO per unit guidance for 2020 in the $1.6 range. Assuming normal distributions, the full year FFO payout would exceed 95%.

Credit profile makes RioCan a relatively good selection among the REIT spectrum

REITs could be considered a vulnerable asset class given the uncertainty around government policies, unemployment trends and the overall pandemic crisis. Despite the resilience at Q3, we've already seen over the second quarter that rent deferrals had an impact on operating performance. Yet, with the help of government assistance programs and RioCan's underwriting policies, I think the REIT has the right tools to navigate the crisis. RioCan holds considerable security deposits (around $C29mios) and letters of credit (>$C5mios) which act as mitigants.

The bulk of RioCan's asset portfolio is also deemed quite defensive in my opinion. At 51%, Toronto contributes to the largest portion of annualized revenue. In my opinion, Toronto's shopping centers which remained open and displayed high occupancy should still yield above average rent. The management team has also completed disposals and sales in retail assets with weaker metrics during the past year. Additionally, the REIT sold in October 50% non-managing interest in its residential rental and retail property in Toronto and Ottawa (Source: Renx). These disposals could allow for more favorable capex spending while maintaining manageable leverage.

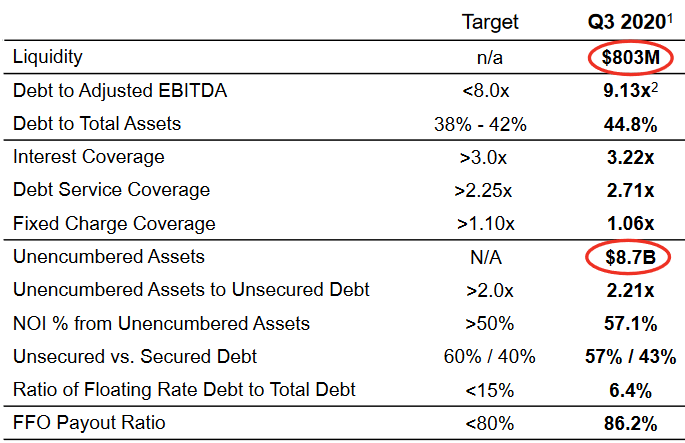

Capital Structure Metrics - Source: RioCan Presentation

The downside of course remains RioCan's leverage, slightly higher than US peers. The REIT's debt/EBITDA averaged 9x at mid-year against 7x for Choice Properties (OTC:PPRQF) and around 5 times for Weingarten Realty Investors (NYSE:WRI) (Source: Respective investor relations). This in my opinion could be a trigger for dividend cuts or a reduction in development activities - which is why I'm not expecting any strong price appreciation over the short/mid term.

From a liquidity perspective, standards look healthy with more than C$80mios in unrestricted cash and more than $800mios in accessible revolving credit.

Valuation and concluding thoughts

Going forward, valuation will depend on a number of factors. Beyond market uncertainty, it remains to be seen whether RioCan will issue more debt or equity. RioCan needs to maintain a fine balance between healthy equity and capitalizing on cash. My rationale of favoring RioCan over many peers is tied to that fine line. The fact that RioCan is trading at a record low FFO multiple despite the good Q3 signals I have mentioned earlier provides a compelling long-term opportunity. RioCan's FFO multiple of around 9x compares with more than 13x for the peer average. RioCan also displays a trailing P/B of 0.6x - in line with the Canadian average despite the higher quality portfolio. From a dividend perspective, the 9.1% yield compares favorably with only H&R (OTCPK:HRUFF) showing similar standards in the Canadian spectrum. Again, a reduction over the next quarter shouldn't be excluded but could be seen positively to reduce leverage and maintain B/S strength.

Trading valuation (2016 to 2020) - Source : RioCan Presentation

Disclosure: I am/we are long RIOCF. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.